.jpg?w=1920&q=75)

If you had to write a cheque today to build a FinTech app, how confident would you feel about the amount on it? For most people, the answer is not very. That’s because FinTech app costs are often talked about in fragments—development here, security there—never as a full picture.

In 2026, building a FinTech app is less about “making an app” and more about building a secure financial system that people can rely on every day. Every login, transaction, and notification carries responsibility. And responsibility comes with a price tag many founders don’t see coming.

This is where confusion usually begins. Someone tells you a FinTech app can be built cheaply. Another warns you it will cost a fortune. Both are partly right—and mostly incomplete. The truth lies in the details: the features you choose, the level of security you need, the regulations you must follow, and the team you trust to build it.

This blog is written for people who want clarity before commitment. No technical jargon. No unrealistic promises. Just a clear, honest breakdown of what it really costs to build a secure FinTech app in 2026—and how to plan your budget without unpleasant surprises later.

What is a Fintech app?

A FinTech app is simply a mobile or web app that helps you manage money using technology. Instead of standing in bank lines or filling long forms, a FinTech app lets you send money, pay bills, take loans, invest, or check balances directly from your phone—anytime, anywhere.

Examples:

- Google Pay / PhonePe – send or receive money

- Paytm – pay bills, recharge, shop

- Zerodha / Groww – invest in stocks or mutual funds

- Banking apps – check balance, transfer money, pay EMIs

So, basically a FinTech app is a digital tool that makes banking and money-related work faster, easier, and paper-free.

Why Fintech App Development Cost Is Not Like Any Other App

Fintech is not just app development with a payment gateway bolted on. It is app development with a layer of financial regulation, security infrastructure, compliance obligations, and third party dependencies that all carry cost, all require maintenance, and all have legal consequences if they are not done right.

Compliance and licensing alone add 20 to 30 percent to your overall budget. Security is not a feature you add in the last sprint. It is an architectural decision baked in from day one. And third party integrations including KYC APIs, payment rails, credit bureaus, and banking core systems all come with integration costs, licensing fees, and ongoing per-transaction or per-user charges.

Here is the uncomfortable truth that most fintech cost blogs gloss over. The initial build is often just 35 to 45 percent of what you will actually spend in the first year. The rest live in the layers that rarely appear in a development proposal.

The Real Cost to Build a Fintech App in 2026: By App Type

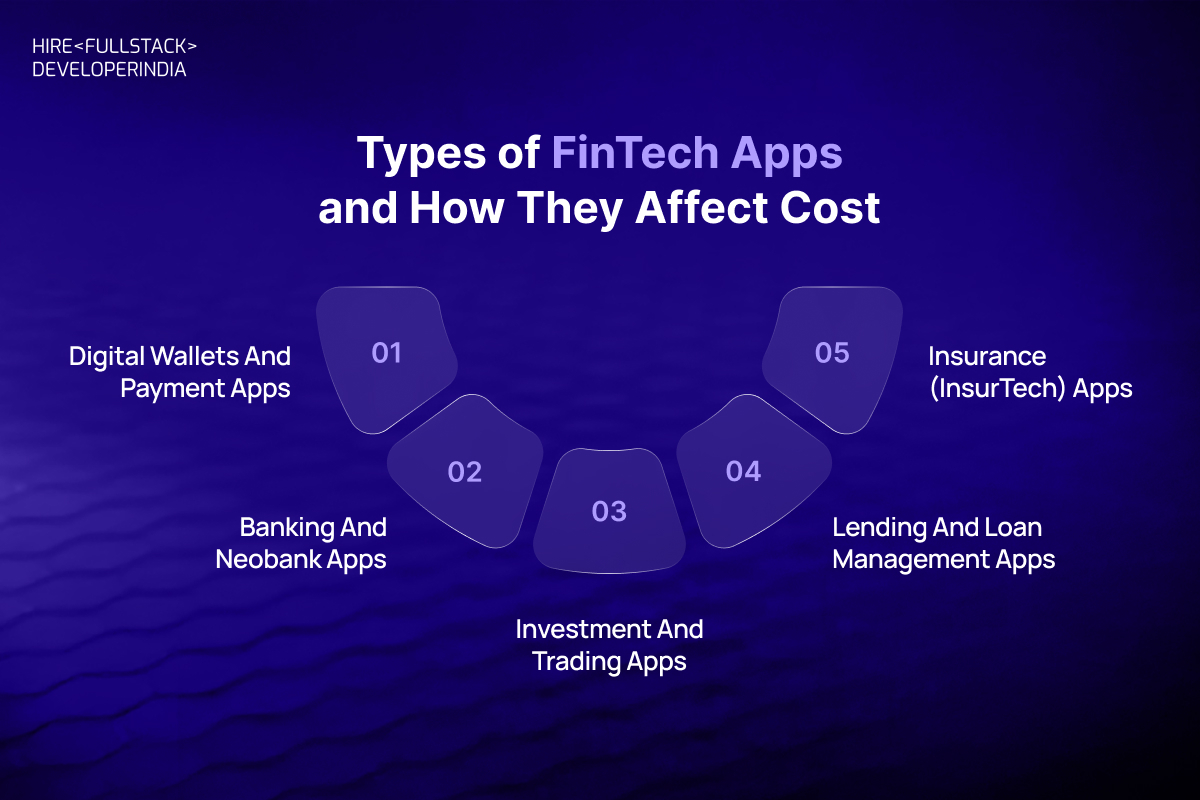

Types of FinTech Apps and How They Affect Cost

The cost to build a FinTech app depends a lot on what kind of app you are creating. Just like building a small shop costs less than building a bank branch, different FinTech apps need different levels of technology, security, and legal approval. More complexity means more cost.

1. Digital Wallets and Payment Apps

These are apps people use to send or receive money instantly.Real-life examples: PhonePe, Google Pay, Paytm, PayPal

Every time a user sends money, the app must talk to banks, check balances, prevent fraud, and confirm the transaction—all in a few seconds. Even a small delay can cause failed payments and angry users.

These apps must be available 24/7 with almost no downtime. If the app stops working for even a few minutes, thousands of transactions can fail. This is why strong servers, real-time processing, and fraud detection systems are required, which increases cost.

2. Banking and Neobank Apps

These apps work like a full digital bank.

Real-life examples: Revolut, N26, Chime

Users can open accounts, get debit cards, check balances, transfer money, and contact support—all inside one app. Because these apps directly replace traditional banks, they must follow strict banking laws and security rules.

The cost is higher because they require deep regulatory compliance, advanced security, and systems that handle large volumes of financial data safely.

3. Investment and Trading Apps

These apps allow users to buy and sell stocks, mutual funds, or cryptocurrencies.

Real-life examples: Zerodha, Robinhood, Coinbase

Prices change every second. The app must show real-time market data and execute trades instantly. Even a small delay can lead to financial loss for users.

These apps are expensive because they need fast systems, licensed market data, and detailed dashboards that help users make decisions quickly.

4. Lending and Loan Management Apps

These apps are used for personal loans, business loans, or BNPL services.

Real-life examples: KreditBee, LendingClub

The app checks user identity, credit score, income details, and repayment history before approving a loan. It also tracks repayments and sends reminders.

Integration with credit bureaus and KYC services increases development and ongoing costs.

5. Insurance (InsurTech) Apps

These apps manage insurance policies and claims digitally.

Real-life examples: Policybazaar, Lemonade

Users can buy policies, upload documents, and file claims through the app. The backend process is complex because it involves risk calculation, approvals, and third-party verification.

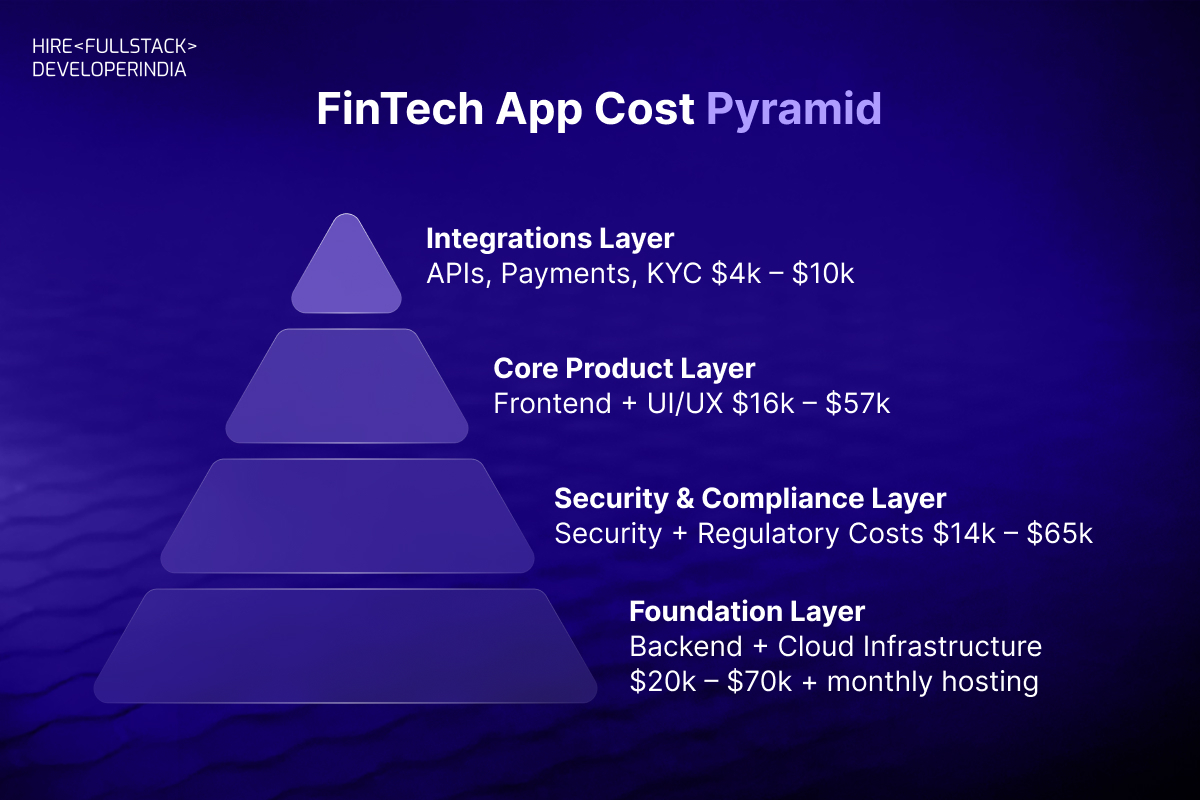

Key Cost Components of a FinTech App

To truly understand the cost to build a FinTech app, you need to look at each cost component separately.

1. Ideation, Market Research, and Planning Costs

Many people underestimate this stage, but it plays a huge role in cost efficiency.

This phase includes:

- Market research

- Competitor analysis

- Feature prioritization

- Risk assessment

- Technical feasibility study

Skipping proper planning often leads to expensive changes later. Investing early helps avoid rebuilding features and restructuring architecture.

Cost range:

$3,000 – $8,000

2. UI/UX Design Costs

FinTech apps must be simple, clear, and trustworthy. Users should understand what is happening with their money at every step.

Design costs include:

- User research and journey mapping

- Wireframes and prototypes

- Visual design for mobile and web

- Accessibility and usability testing

A poor design leads to user errors, support issues, and low adoption. Good design reduces operational costs over time.

Cost range:

- Basic design: $4,000 – $6,000

- Advanced UX with testing: $7,000 – $12,000

3. Frontend Development Costs

Frontend development is what users see and interact with. It includes mobile apps, web dashboards, and admin panels.

Cost factors:

- Platform choice (iOS, Android, Web)

- Cross-platform vs native development

- Real-time data updates

- Performance optimization

FinTech apps require smooth performance and accurate data display, which increases development effort.

Cost range:

- Single platform: $12,000 – $20,000

- iOS + Android + Web: $25,000 – $45,000

4. Backend Development Costs

The backend is the backbone of any FinTech app. This is where most of the complexity lies.

Backend costs include:

- Business logic development

- Database architecture

- API development

- Payment processing logic

- Transaction management

A weak backend can lead to transaction failures and data inconsistencies. This is why businesses often hire full-stack developers for FinTech projects who understand both frontend and backend systems.

Cost range:

- Basic backend: $20,000 – $35,000

- Scalable, secure backend: $40,000 – $70,000

5. Security Implementation Costs

Security is the biggest cost driver in FinTech app development.

Security measures include:

- Data encryption (at rest and in transit)

- Secure authentication and authorization

- Multi-factor authentication

- Fraud detection systems

- Secure API gateways

- Session management

Regular penetration testing and vulnerability assessments are also required. These are recurring costs, not one-time expenses.

Cost range:

- Standard security: $8,000 – $15,000

- Advanced security & fraud systems: $18,000 – $35,000

6. Compliance and Regulatory Costs

In 2026, regulatory requirements are stricter than ever.

Common compliance needs:

- KYC (Know Your Customer)

- AML (Anti-Money Laundering)

- PCI-DSS for payment data

- GDPR and data privacy laws

- Country-specific financial regulations

Compliance involves legal consultation, documentation, audits, and technical implementation. This significantly increases the FinTech app development cost but is mandatory.

Cost range:

- Initial compliance setup: $6,000 – $12,000

- Advanced compliance & audits: $15,000 – $30,000+

7. Third-Party Integrations

Most FinTech apps rely on external services.

Examples include:

- Payment gateways

- Banking APIs

- Identity verification services

- Credit scoring APIs

- SMS and email services

Each integration has development costs, testing costs, and ongoing usage fees.

Development cost:

- $4,000 – $10,000

Ongoing API usage fees:

- $500 – $3,000 per month (varies by volume)

8. Cloud Infrastructure and Hosting Costs

FinTech apps require secure and scalable infrastructure.

Infrastructure costs include:

- Cloud servers

- Databases

- Load balancers

- Backup and disaster recovery systems

- Monitoring and logging tools

As your user base grows, infrastructure costs grow as well. Planning scalability early helps control long-term expenses.

Cost range:

- Early stage: $300 – $800/month

- Growth stage: $1,500 – $4,000/month

9. Quality Assurance and Testing Costs

Testing is not optional for FinTech apps.

Testing types include:

- Functional testing

- Security testing

- Performance testing

- Compliance testing

- User acceptance testing

This stage ensures reliability and prevents costly failures after launch.

Cost range:

- $6,000 – $12,000

10. Maintenance and Ongoing Support Costs

The cost to build a FinTech app does not end at launch.

Ongoing costs include:

- Bug fixes

- Security updates

- Compliance updates

- Server costs

- Feature enhancements

Maintenance usually accounts for a significant percentage of the initial development cost each year.

Annual maintenance cost:

- 15% – 25% of initial development cost

Team Structure and Hiring Costs

One of the biggest decisions that affects your FinTech app development cost is who you hire to build it. The same app can cost very different amounts depending on the team structure you choose.

Option 1: In-House Team

This means hiring your own employees full-time.

You would need developers, designers, testers, and security experts on your payroll. While this gives you full control, it is also the most expensive option.

Realistic cost:

- $120,000 – $250,000 per year (salaries, benefits, tools, office costs)

This option is usually suitable only for large companies or well-funded startups.

Option 2: Freelancers

Freelancers are individuals hired for specific tasks.

They may charge less, but managing multiple freelancers can be difficult. Security practices may vary, and coordination often becomes a challenge—especially for sensitive FinTech projects.

Realistic cost:

- $25 – $60 per hour

- Total project cost: $40,000 – $80,000 (with higher risk)

This option works for small experiments but is risky for full-scale FinTech apps.

Option 3: Development Agencies (Most Preferred)

A FinTech development agency provides a complete, managed team. This is why many companies choose to hire full-stack developers for FinTech through experienced development companies.

You get structured processes, better security standards, and a single point of accountability.

Realistic cost:

- $50,000 – $150,000 depending on complexity

Typical FinTech Development Team Includes:

- Full-stack developers – build frontend and backend

- UI/UX designers – make the app simple and user-friendly

- QA engineers – test the app for bugs and failures

- DevOps specialists – manage servers and deployment

- Security experts – protect data and prevent fraud

Choosing the right team is not just about cost—it’s about building a secure, reliable app users can trust.

How Location Affects FinTech App Development Cost

Many people are surprised to learn that where your development team is located can change your FinTech app cost significantly, even if the app features remain exactly the same.

This happens because development costs depend on local salary levels, living costs, and market demand for tech talent. A developer in one country may charge three times more than an equally skilled developer in another country.

If you hire a development team in countries like the United States, Canada, or Western Europe, the cost is usually higher. Developers in these regions charge premium rates because of higher living expenses and strong local demand.

Average cost in these regions:

- $80 – $150 per hour

- Full FinTech app cost: $180,000 – $350,000+

On the other hand, regions such as India, Eastern Europe, and parts of Southeast Asia offer strong technical talent at more affordable rates. Many developers here work on global FinTech projects and follow the same security and compliance standards.

Average cost in these regions:

- $25 – $50 per hour

- Full FinTech app cost: $50,000 – $150,000

This does not mean cheaper quality. It simply means lower operational costs. By hiring from cost-efficient regions, businesses can optimize their budget without compromising on security, performance, or reliability.

The key is choosing an experienced FinTech development partner, not just the cheapest option

Estimated Cost Breakdown for a Secure FinTech App in 2026

A secure FinTech app is not a one-time expense. While the initial build may cost anywhere between $80,000 to $150,000 for most startups, the real investment continues every year through security updates, compliance checks, infrastructure, and maintenance.

Common Mistakes That Increase Costs

Many founders make avoidable mistakes:

- Skipping security planning

- Underestimating compliance

- Choosing the wrong tech stack

- Cutting costs on testing

These mistakes often lead to higher expenses later.

What Features Actually Drive the Cost of Building a Fintech Mobile App

The most important thing to understand about fintech feature costs is that no feature costs only what it costs to build. Every feature that touches money, user identity, or a financial decision carries a compliance multiplier. That multiplier gets applied on top of the base development cost and it rarely, if ever, appears in a standard feature estimate.

Core Feature Costs With Their Compliance Reality

The compliance multiplier is not padding. It is the legal and technical work that makes each feature lawful to operate in a regulated financial environment. The feature that looks like a two week sprint on the estimate sheet is often a six week project once you account for the compliance layer around it.

The Features Nobody Mentions Until It Is Too Late

Beyond the main feature list, there are three cost areas that almost never appear in a standard development proposal but will absolutely affect your fintech app development budget.

- Regulatory reporting modules. If your app handles transactions above a certain threshold in most jurisdictions, you need automated reporting to regulatory bodies. Building this cleanly adds $15,000 to $40,000 to your budget.

- Immutable audit trails and tamper-proof logging. Every transaction, every login, every data change needs a traceable log that regulators can inspect. This is a compliance requirement, not a nice-to-have, and it adds $8,000 to $20,000 to your build

- Graceful degradation systems. What happens when your payment gateway is down mid-transaction? When does your KYC API time out mid-onboarding? Engineering these failure scenarios properly so users do not lose money or get stuck requires real effort that gets skipped in early builds and causes expensive incidents later.

How to Optimize Your FinTech App Budget

Building a FinTech app does not mean you have to spend blindly. Smart planning can help you control costs while still building a secure and reliable product. The key is knowing where to invest and where to wait.

1. Build an MVP First (Start Small, Then Grow)

An MVP (Minimum Viable Product) is the simplest working version of your app. Instead of launching with 20 features, you start with 5 that truly matter.

For example, if you are building a payment app, focus only on sending and receiving money first. Fancy dashboards and advanced analytics can come later.

How this saves money:

You avoid spending $150,000 upfront and instead start with $40,000–$70,000, while testing real user demand.

2. Prioritize Essential Features Only

Not every idea needs to be built on day one. Many founders waste money building features users don’t even use.

Ask one simple question: Does this feature help users move money safely and easily? If not, it can wait.

How this saves money:

Less development time, lower testing costs, and faster launch.

3. Use Scalable Cloud Infrastructure

Instead of buying expensive servers upfront, use cloud services that grow as your users grow.

Start small. Upgrade only when traffic increases.

How this saves money:

You pay only for what you use—starting at $300–$800 per month instead of large upfront infrastructure costs.

4. Work With Experienced FinTech App Development Services

Experienced teams already know security rules, compliance needs, and common mistakes.

How this saves money:

Fewer errors, no rework, and faster development—saving both time and long-term costs.

How AI Integration Influences FinTech App Cost

In 2026, many FinTech apps are adding AI (Artificial Intelligence) to become smarter, faster, and more user-friendly. AI can help detect fraud, provide personalized financial advice, automate customer support, or predict spending trends. While these features improve your app, they also increase the overall cost.

Why AI Adds to Cost

- Complex Development

AI requires additional coding and specialized algorithms. Developers need to build systems that can learn from data and make decisions automatically, which takes more time and expertise than a regular app. - Data Collection & Management

AI depends on large volumes of data. Collecting, storing, and securing this data increases costs for infrastructure and compliance. - Specialized Talent

AI features require experts like data scientists and machine learning engineers, who are usually more expensive than standard developers. - Continuous Learning & Maintenance

AI systems need regular updates and retraining to remain accurate. This adds to ongoing maintenance costs.

Real-Life Examples of AI in FinTech Apps

- AI Chatbots – Automated customer support that answers common queries instantly.

Estimated extra cost: $5,000 – $10,000 - Fraud Detection Systems – AI monitors transactions in real time to spot suspicious activity.

Estimated extra cost: $15,000 – $40,000 - Personalized Financial Advice – AI suggests investments or savings plans based on user behavior.

Estimated extra cost: $20,000 – $50,000 - Predictive Analytics for Loans – AI predicts creditworthiness to speed up loan approvals.

Estimated extra cost: $25,000 – $60,000

Average Cost to Build a Secure FinTech App in 2026 (Quick Overview)

Let’s talk straight—building a FinTech app isn’t cheap, and adding AI makes it a bit pricier. Here’s a realistic idea of what you might spend:

- Basic FinTech MVP (no AI): $40,000 – $70,000

- Mid-level FinTech app (with simple AI like chatbots or smart notifications): $90,000 – $160,000

- Advanced / Enterprise app (AI for fraud detection, personalized advice, or predictive insights): $200,000 – $400,000+

Why the difference? It depends on what your app can do, how secure it is, and which AI features you include. A simple chatbot costs much less than an AI system that predicts spending patterns or detects fraud in real time.

The big idea: AI can make your app smarter and more useful for users, but it also increases both the development and ongoing maintenance costs. Planning these features early helps you keep your budget under control and avoid surprises later.

Final Thoughts

Creating a secure FinTech app in 2026 is more than just writing code. It’s about making sure your app is safe, reliable, and compliant with financial rules. Add AI features, and you’re also giving your users smarter tools, like fraud detection or personalized financial tips—but this does affect the cost.

The key is to plan carefully. Start with the most important features, choose a skilled development team, and think about security, compliance, and AI from the beginning. This way, you avoid expensive mistakes and surprises later.

At the end of the day, a well-built FinTech app is an investment in trust and growth, not just a project. When done right, it keeps your users confident, helps your business scale, and gives you a strong foundation to add new features and innovations in the future.